Final 2026 Open Enrollment Report: Household Income (200 - 400% FPL)

Sat, 04/11/2026 - 4:04pm

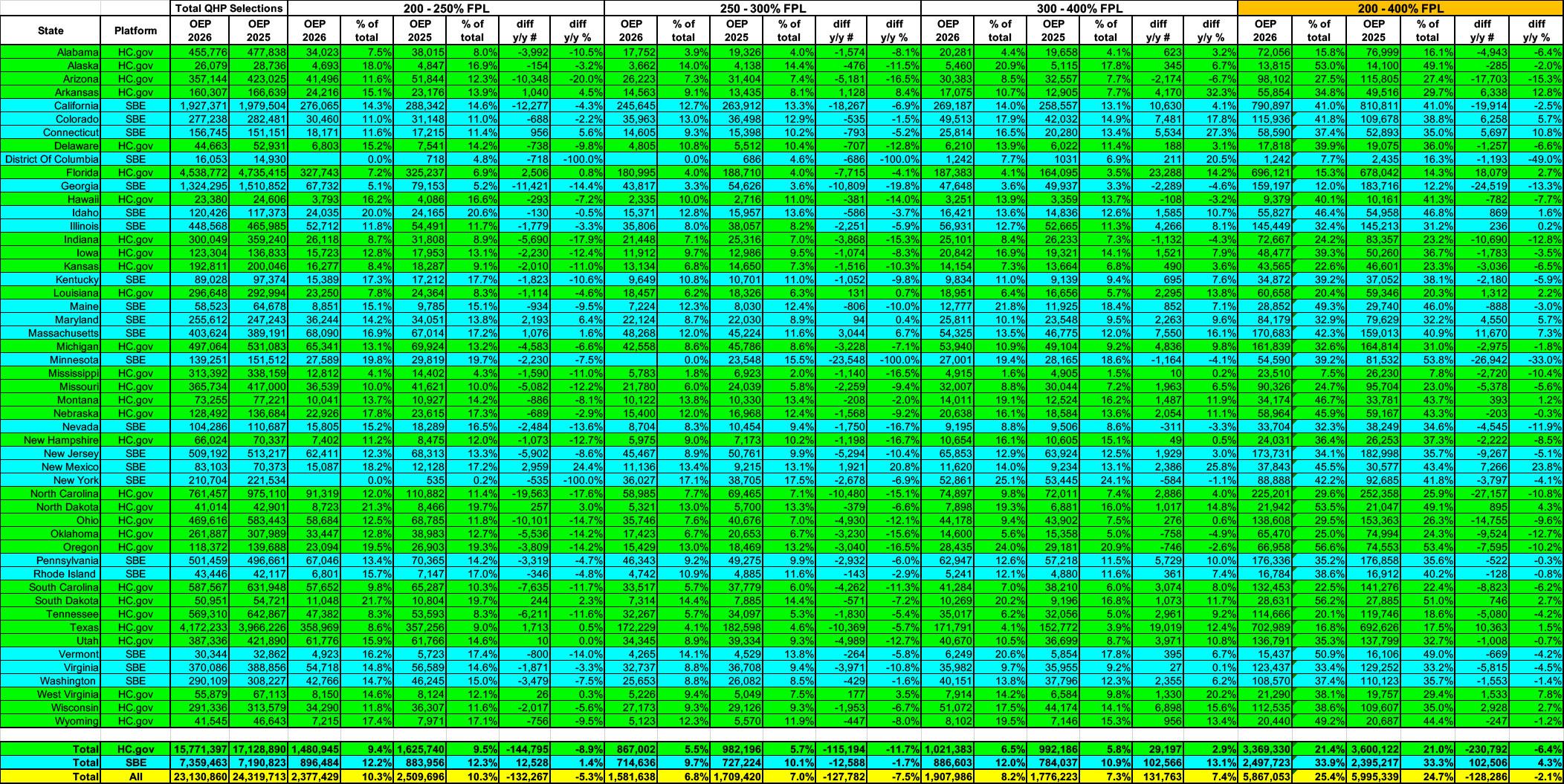

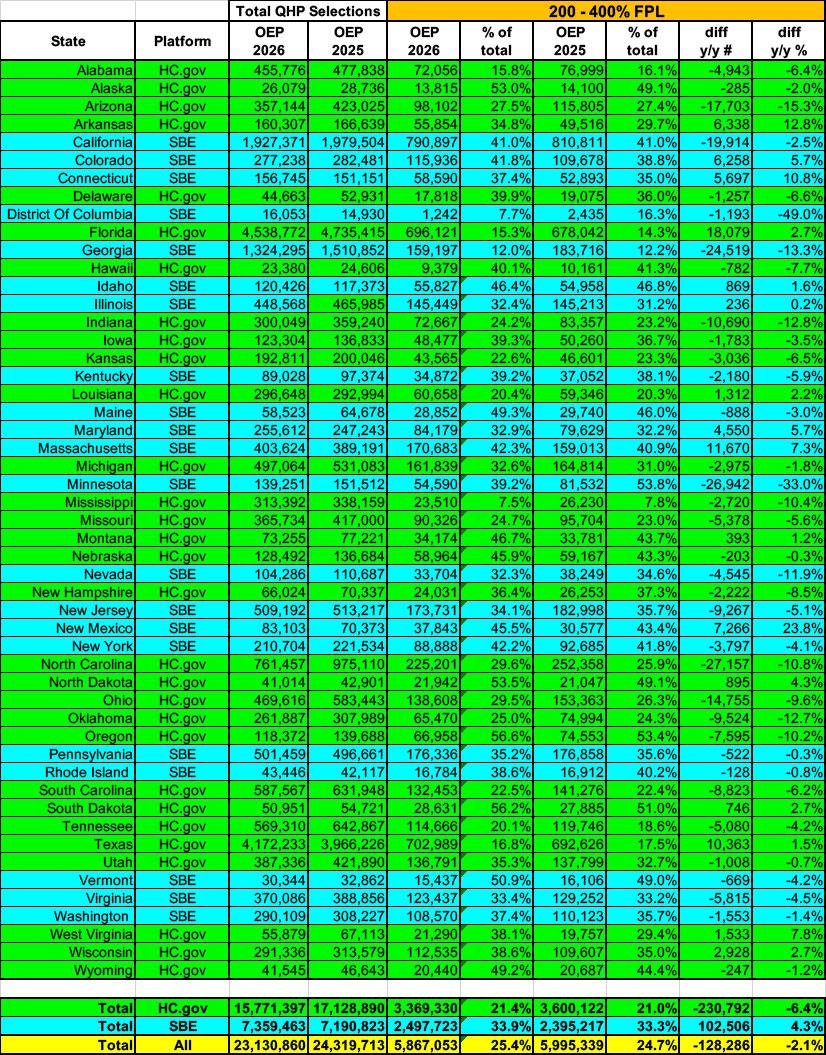

Next, let's look at the 200-400% FPL bracket. These make up just over 1/4th (25%) of total ACA exchange enrollment this year, up slightly from last year.

Overall enrollment in this bracket only dropped by about 2.1% (128,000 people), which makes sense for several reasons:

- First, they were the least-impacted by the enhanced subsidies expiring (most of them still saw their premiums jump dramatically, just not as dramatically as those below 200% FPL or over 400% FPL)

- Second, the Trump Regime policy change making recent (under 5 years) documented immigrant residents ineligible for federal tax credits doesn't really apply to this population anyway.

However, there's a third reason for the relatively small drop-off in this income range which I'll address below....

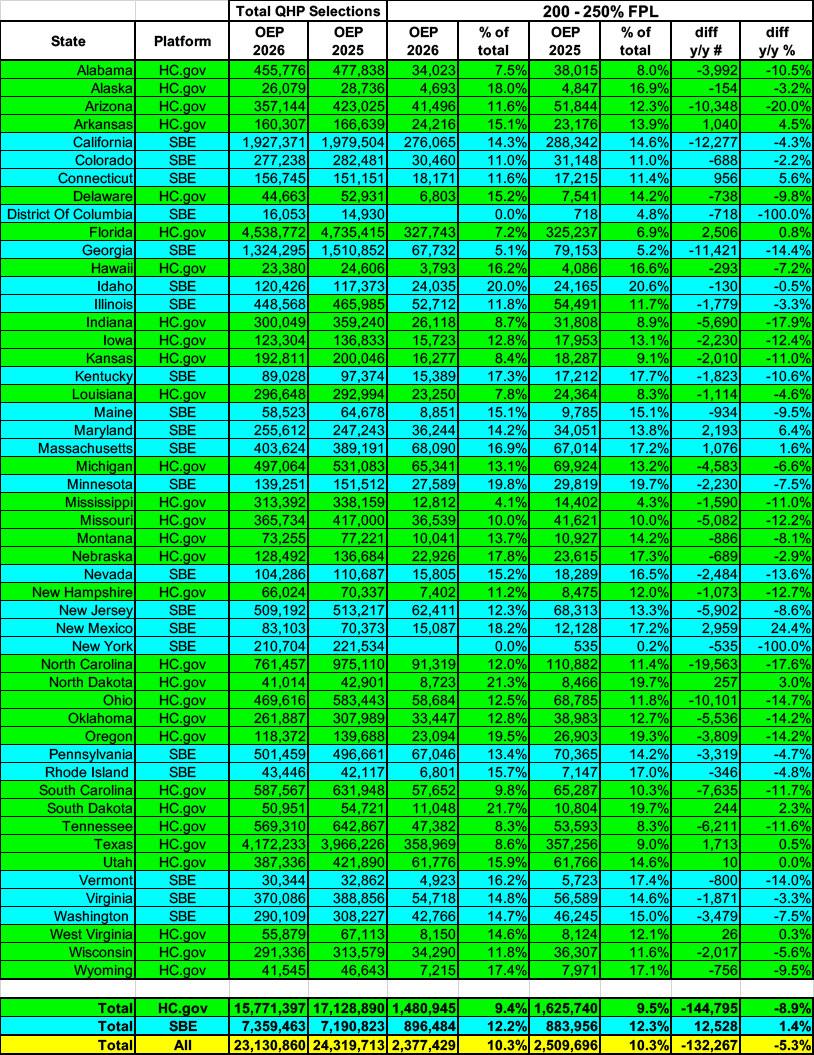

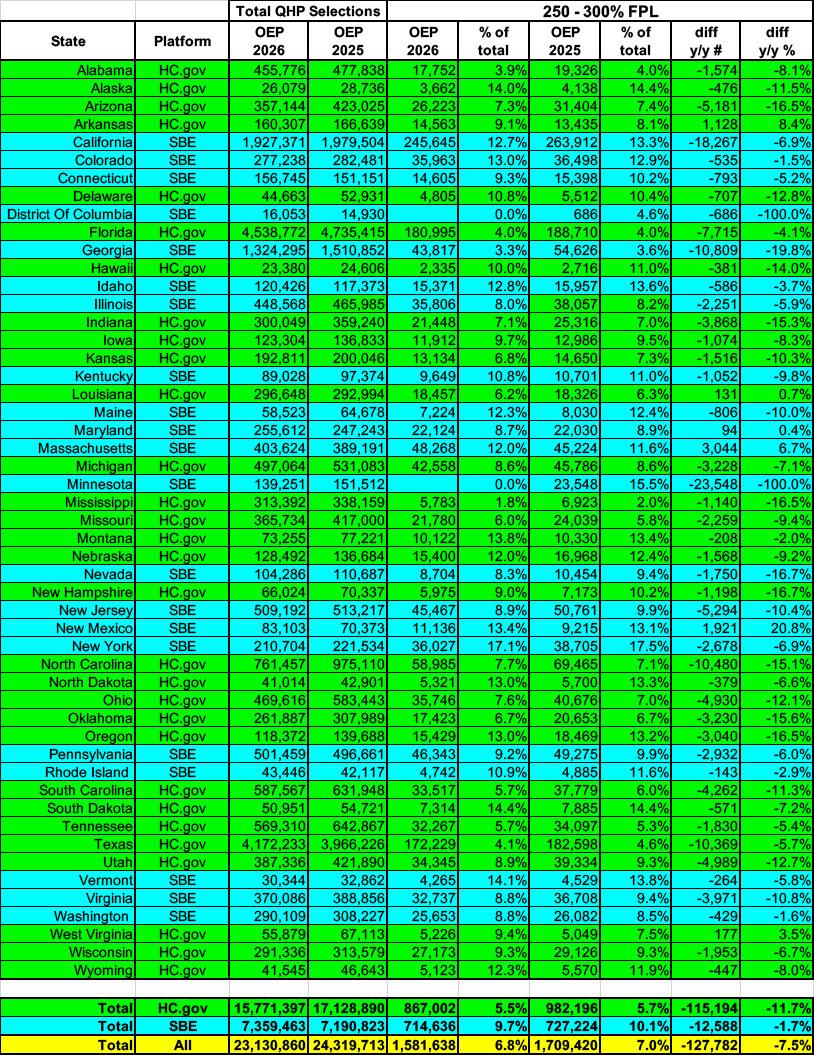

When you further break the 200 - 400% FPL range out into smaller chunks, you'll see that enrollment dropped at a much higher level from 200 - 250% FPL: There's 132,000 fewer enrollees in this range, a drop of 5.3%...and if you look at the 250 - 300% FPL range, it's an even steeper drop: Another ~127,000 people, or 7.5% fewer enrollees...

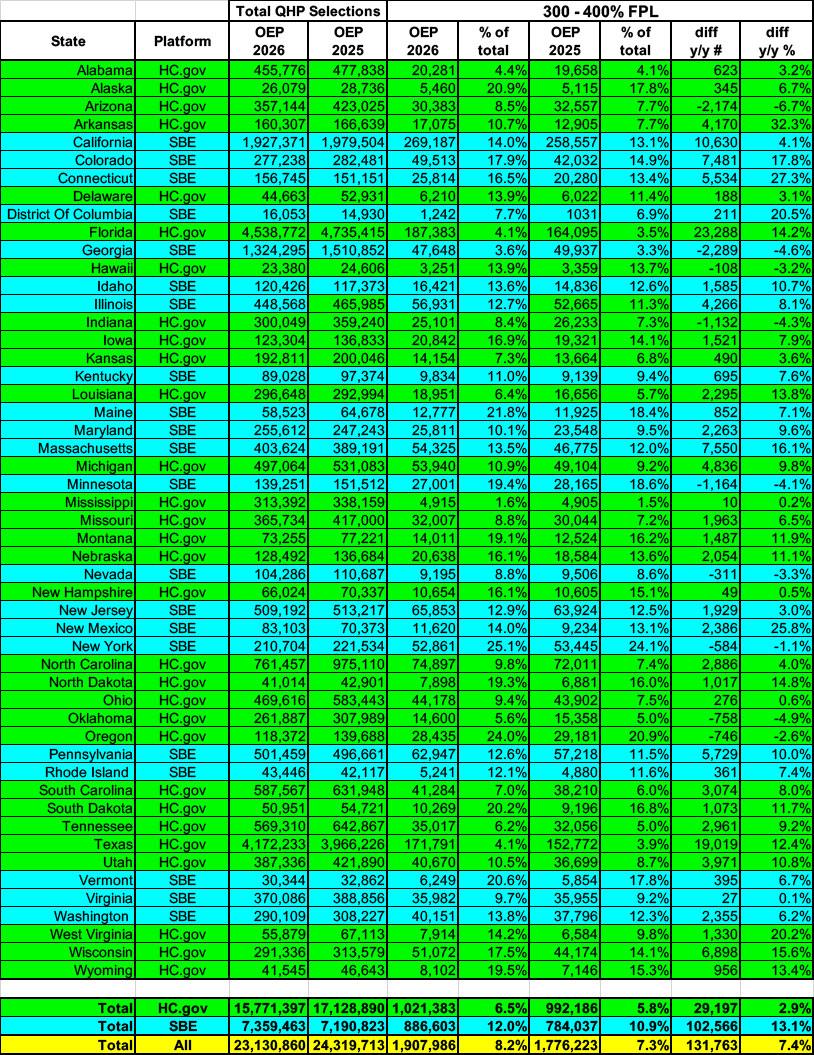

HOWEVER, if you look at the 300 - 400% FPL range, it's a completely different story: Here, enrollment actually increased by pretty much the same amount that it dropped in each of the prior two brackets: ~132,000 more enrollees, an increase of 7.4% vs last year!

So what's going on here? Well, keep in mind that while the ACA subsidy formula became much less generous for enrollees who earn less than 400% of the Federal Poverty Level (FPL), they completely expired for anyone with a household income over 400% FPL.

Now, if you earn, say, a half a million dollars a year, having to pay full price isn't that big of a deal (unless you're in your early 60's and live in West Virginia, Alaska or Wyoming, where a 64-yr old couple could have to pay a whopping ~$60K/year in premiums alone this year).

For households which earn more than ~$130K but less than around $250K/year, however, that can still be a massive hit to their household budget...and if you earn just barely more than 400% FPL, it can be devastating.

For example, consider a 63-yr old couple living in Lansing, Michigan who earns $90,000/year.

Last year they would have had their premiums for the benchmark Silver ACA plan capped at no more than 8.5% of their income: $7,650/year, or $638/month in premiums.

This year, however, that same couple earning exactly the same amount has to pay full price...which, in Lansing, MI, happens to be a whopping $2,695/month in premiums alone. That's $32,340/yr in premiums, or a stunning 36% of their gross income!

Fortunately for some of these folks, there are several perfectly legal ways to drop your official MAGI income below 400% FPL, as explained by my friend & colleague Louise Norris:

A lower income and more adjustments to income will reduce MAGI. You should consult your tax advisor to consider the available deductions/adjustments on your tax return that are above the line that shows your AGI since reductions to your AGI will also reduce your ACA-specific MAGI.

Tax-deductible contributions to a traditional individual retirement account (IRA) will reduce your ACA-specific MAGI. Your tax advisor should be able to explain the details of this to you, including how to determine whether you’re eligible to make tax-deductible contributions to a traditional IRA.

In addition, your tax advisor can explain how contributing to an employer-sponsored pre-tax retirement plan like a 401(k) will lower your ACA-specific MAGI.

...If you’re self-employed, your tax advisor can advise whether it is in your best interest to set up a self-employed retirement plan such as a SEP IRA, SIMPLE IRA, or Solo 401(k). Talk with your tax advisor to see if one makes sense for you. Keep in mind that these retirement plans for self-employed people have contribution limits that are potentially higher than those of traditional IRAs allowing people to reduce their MAGI by a larger amount than a traditional IRA would allow.

If you have an HSA-eligible high-deductible health plan (HDHP), contributions to an HSA will reduce your ACA-specific MAGI. Your tax advisor should be able to answer any questions you have about this. It's important to note that starting with the 2026 plan year, all Bronze and catastrophic plans purchased in the health insurance Marketplace will be considered HDHPs. So if you enroll in one of these plans, you'll be eligible to contribute to an HSA, as long as you don't have any additional major medical coverage.

Self-employed people may also deduct their health insurance premiums, which may lower their MAGI, but it gets a bit complicated if that’s the factor that makes you eligible for a premium subsidy.

In this couple's case, they'd have to knock their MAGI income below $86,560, which means coming up with at least $3,440 in adjustments. If they're able to put $3,500 into an HSA or an IRA, it will nudge them below the 400% FPL threshold, capping their premiums for the benchmark plan to $8,964/yr or $747/month. This would still be $1,314 more than last year, but that would still be way better than having to pay an additional $24,690! In short, for this example, putting $3,500 into an eligible account would save this couple over $23,000.

This is almost certainly what explains the sudden surge in households projecting a 300 - 400% FPL income range in 2026. It doesn't mean that all of them will end up being successful, mind you; many of them will likely end up over the 400% FPL threshold after all, in which case they'll have to pay back ALL of the federal subsidies they receive this year when they file their 2026 taxes next spring (ouch).

However, it's absolutely worth giving a shot for those who earn less than, say, 450% FPL, give or take.

In any event, given that the drop-off in both the 200 - 250 and 250 - 300% brackets range from 5.3 - 7.5%, I think it's safe to assume that enrollment in the 300 - 400% range would have dropped by a similar amount if not for the "keep it under 400" factor, which suggests that perhaps ~250,000 enrollees who normally earn more than 400% FPL are attempting to keep their MAGI income below that threshold this year.

Advertisement