One of the most insanely stupid provisions of the ACA just became *slightly* less stupid

Tue, 03/17/2026 - 4:41pm

In U.S. politics, the Hyde Amendment is a legislative provision barring the use of federal funds to pay for abortion, except to save the life of the woman, or if the pregnancy arises from incest or rape. Before the Hyde Amendment took effect in 1980, an estimated 300,000 abortions were performed annually using federal funds.

Nearly 9 years ago, I took a closer look at one of the more absurd provisions of the Affordable Care Act which relates directly to the Hyde Amendment, specifically in light of this story from Health Affairs:

On October 6, 2017, the Center for Consumer Information and Insurance Oversight (CCIIO) released a new bulletin regarding the coverage of abortion by qualified health plans (QHPs) sold through the ACA marketplaces. The bulletin provides additional guidance on how rules and restrictions on abortion coverage will be enforced by federal officials beginning in plan year 2018.

Coverage of abortion was one of the most contentious and last resolved issues in the debate over the ACA. The final Senate compromise, which was adopted as part of the ACA, largely reinforces the Hyde Amendment, which has been included in annual Congressional appropriations legislation since the 1970s and prohibits the use of federal funds for abortion services unless the pregnancy is a result of rape or incest, or would endanger the woman’s life (non-Hyde abortions).

The ACA allows the coverage of abortion services through the marketplaces but includes a number of restrictions and requirements that insurers must follow before covering non-Hyde abortions. Many, though not all, of these restrictions are outlined in Section 1303 of the ACA, which includes specific rules related to the coverage of abortion services by QHPs and has been the subject of previous litigation. In particular, Section 1303:

- Prohibits insurers from using any portion of premium tax credits or cost-sharing reduction payments to pay for non-Hyde abortion services;

- Requires insurers to inform consumers in their summary of benefits and coverage that the QHP they are considering includes coverage of non-Hyde abortion services; and

- Requires insurers that cover non-Hyde abortions to determine the cost of and then separately collect and segregate funds for non-Hyde abortion services.

Section 1303 further specifies that individuals who purchase insurance that covers abortions must pay at least one dollar into a separate account specifically designated for abortion. These segregated accounts are designed to help ensure that the accounts are 1) funded solely by the enrollee’s premium (rather than by the premium tax credit) and 2) used exclusively to fund non-Hyde abortion services.

Section 1303 also allows states to ban the coverage of abortions by QHPs sold through the marketplaces: to date, twenty-six states have done so. In an additional six states, no marketplace plans offered coverage for abortion during the 2016 plan year. Two states—California and New York—require health plans to cover abortions, subject to an exception for multistate plans, at least one of which in each state must offer insurance without abortion coverage.

The good news is that the number of states which legally require ACA marketplace insurance plans to coverage abortion has increased to 13 since this was published; it now includes California, Colorado, Delaware, Illinois, Maine, Maryland, Massachusetts, Minnesota, New Jersey, New York, Oregon, Vermont and Washington, while the number of states which ban them has dropped to 25 (I'm not sure which one has dropped from that list).

The bad news, of course, is that since I first wrote about this provision, the Supreme Court has overturned Roe vs. Wade, and 13 states have made abortion illegal in practically all cases.

In any event, the actual wording of Section 1303 clarifies that the "separate account" payment has to be at least $1.00 per month per enrollee:

(C) <<NOTE: Cost estimate.>> Actuarial value of optional service coverage.-- (i) In general.--The Secretary shall estimate the basic per enrollee, per month cost, determined on an average actuarial basis, for including coverage under a qualified health plan of the services described in paragraph (1)(B)(i). (ii) Considerations.--In making such estimate, the Secretary-- (I) may take into account the impact on overall costs of the inclusion of such coverage, but may not take into account any cost reduction estimated [[Page 124 STAT. 171]] to result from such services, including prenatal care, delivery, or postnatal care; (II) shall estimate such costs as if such coverage were included for the entire population covered; and (III) may not estimate such a cost at less than $1 per enrollee, per month.

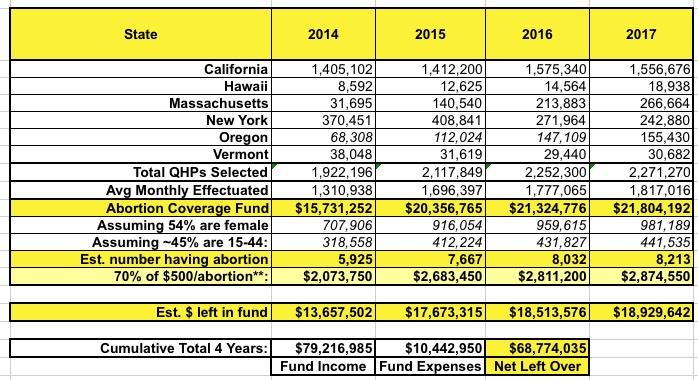

An actuary friend of mine noted at the time that from a pure cost perspective, $1 per member per month added up to a lot more money being put into these segregated funds than would ever actually be used to pay for abortions. I started running the numbers and came up with a very rough guesstimate; at the time, I estimated that the amount of actual premium revenue added worked out to something like $79 million from 2014 - 2017. I then did some more calculations and concluded that of that, perhaps $10.4 million was actually used to pay for abortion services for enrollees in those plans:

In other words, there was likely nearly $69 million just sitting around in those bank accounts, presumably gathering interest, which couldn't be used for any other purpose until the end of time (or until a policy change). Several years later I updated my estimates to perhaps as much as $200 million nationally as of 2021. As I said at the time:

The ACA explicitly states that those remaining funds cannot be used for any other purpose, which means it can't go towards other types of claims...but I also assume it means the carriers can't use it to pay employee salaries, to buy out other companies, as part of an investment portfolio or anything else. It's basically just a checking account.

Well, it's been another 5 years, which has also included dramatic increases in ACA plan enrollment; effectuated enrollment in 2025 averaged nearly twice as much as in 2021.

I'm not going to bother doing more number crunching on this, but I think it's safe to say that at least another $200 million or so has been added to these "Abortion Funds" across the country, for perhaps $400 million or so total, give or take (?).

As insanely offensive and stupid as this policy was at the time, it almost got even worse during the first Trump administration:

Trump administration proposes new rule requiring separate premium bills for abortion coverage

The Trump administration wants insurers that offer plans through Access Health CT, Connecticut’s Affordable Care Act exchange, and other exchanges nationwide, to send people separate monthly bills for the cost of their abortion coverage — in addition to the bill they get for their regular premium costs.

This means people would receive two separate bills in the mail or electronically — one to cover the premium costs for services such as primary care, mental health, maternity, etc. — and another one solely for the cost of their abortion coverage premium.

People on the exchange would also have to make two separate payments for these bills, according to a proposed rule recently released by the Centers for Medicare and Medicaid Services (CMS).

As I noted at the time:

...Between printing, postage, processing and so forth, there's a good chance it will cost the carriers more than $1.00 per enrollee anyway, which will lead some of them to drop abortion coverage from their policies altogether, which is of course the entire point.

In addition, this will humiliate and embarrass many women enrolled in the policies as they're further degraded by having an extremely personal and sensitive medical issue specifically called out. And of course I guarantee that thousands of people will end up receiving late payment notices (potentially even losing their coverage eventually) even when they pay their premiums regularly because they didn't notice the second invoice for a mere $1.00 that shows up each and every month.

An article from HealthAffairs about this proposal even went into the cost estimates of such a policy:

HHS estimates that 75 QHP insurers offered a total of 1,111 plans covering non-Hyde abortions in 17 states; the new burden of separate invoices and billing for these insurers would cost about $1.6 million annually. The proposed rule would also affect an estimated 1.3 million consumers nationwide who would need to separately pay a non-Hyde premium. The estimated burden on consumers is $30.8 million, excluding the cost of “consumer learning” as consumers try to navigate two separately mailed bills.

The good news, such as it is, is that this "separate check in a separate envelope" rule never ended up actually going into effect; there was a lawsuit filed (naturally) and a federal judge enjoined the rule in July 2020...I'm assuming it was stayed long enough for President Biden to take office and reverse the policy before it kicked in anyway.

Anyway, that's where things have stood for the past 12 years...until now.

Back in December, the Centers for Medicare & Medicaid Services (CMS) sent out a Frequently Asked Questions (FAQ) to interested parties regarding this specific issue:

December 9, 2025

Frequently Asked Questions (FAQs) on Usage of Funds in Section 1303 Segregated Accounts by Qualified Health Plan (QHP) Issuers in the Individual Market

Summary: Section 1303 of the Patient Protection and Affordable Care Act (ACA), as implemented at 45 C.F.R § 156.280, establishes requirements with respect to coverage of certain abortion services by QHP issuers in the individual market. Section 1303 of the ACA and 45 C.F.R § 156.280 require individual market QHP issuers that cover abortion services for which federal funding is prohibited (non-Hyde abortion services) to collect two separate payments from each enrollee per month: one for the actuarial value (AV) of coverage of non-Hyde abortion services (at least $1 per enrollee per month), and one for all other covered services.

Issuers must deposit these separate payments into segregated accounts and maintain the segregation of such funds. We refer to these segregated accounts as the “non-Hyde abortion segregated account” and the “segregated account for all other covered services,” respectively, when referring to these accounts individually. When referring to both accounts collectively, we use the terms “Section 1303 segregated accounts” or “segregated accounts.”

The Centers for Medicare & Medicaid Services (CMS) understands that funds in many QHP issuers’ Section 1303 segregated accounts holding payments received for coverage of non-Hyde abortion services have accumulated year over year because the AV of coverage of non-Hyde abortion services is generally less than $1 per enrollee per month. These segregated accounts may also generate interest, further increasing the total amount accumulated.

These FAQs discuss Section 1303 of the ACA and 45 C.F.R § 156.280 requirements in greater detail and provide guidance on how QHP issuers in the individual market can use the accumulated funds in their Section 1303 segregated accounts, and the non-Hyde abortion segregated accounts in particular.

The FAQ goes into some wonky detail about usage of these funds, which resulted in an analysis by Manatt, Phelps & Phillips, LLP in February 2026, which concluded that:

Summary:

Pursuant to recent federal guidance, after a given coverage year has concluded, any unspent Section 1303 segregated abortion premiums can be treated the same as any other source of premium revenue. Unspent individual market 1303 premium revenue can be transferred to the general premium revenue account(s), subject to a state’s laws governing premium revenue....Federal Guidance:

On December 9, 2025, CMS issued guidance noting that QHP issuers can treat unspent segregated abortion premium premiums as any other form of premium revenue after the coverage period for when the premium was collected ends....To utilize these funds for purposes other than non-Hyde abortion services, QHP issuers must move the unspent premium funds in their non-Hyde abortion segregated accounts to general issuer-managed accounts.” Further, the guidance defers to QHP issuers (and presumably states) to determine how to utilize these unspent premium funds after the conclusion of the plan year after all claims are paid or accounted for to best meet their needs and the needs of their enrollees, consistent with any applicable federal and state requirements.

Uses of Unspent Premium Dollars:

Because unspent premium dollars are treated like all other premium revenue, the QHP issuer can use these dollars in other ways, subject to their medical loss ratio requirement, or direct those funds to the state. Therefore, in addition to using unspent premium dollars on abortion services, issuers could also use dollars on a broad range of activities, including as directed by the state if the funds are moved outside of the separate accounts....Future state programs:

The federal guidance makes clear that QHP issuers and states can determine the use of unspent revenue after the conclusion of the plan year (subject to federal laws). Given actions taken against Maryland, using unspent revenue to fund abortion services outside the current accounts is risky but could likely still be accomplished given the other state’s existing program. There does not appear to be anything in the guidance to prohibit states from using unspent segregated funds to to fund other coverage policies as long as those funds are moved out of the accounts.The amount of accumulated funds likely varies significantly by state and by QHP issuers. Given the lack of guidance, it would be reasonable for different issues to have historically taken different approaches to the fund. State insurance commissioners could do a data call to determine the current state of fund accumulation in order to assess the feasibility of capturing these funds (through assessments or other transfers) to fill coverage gaps created by H.R. 1 and other federal actions.

The Manatt analysis also offers some insight into my back-of-the-envelope math about just how much money we're talking about here:

...Maryland stated that the balance of their segregated abortion account was about $25 million in February 2025, and nets about $3 million additional.

Maryland has a little over 1% of total ACA enrollment nationally, give or take. If you limit this to just the 13 states which mandate abortion coverage for all ACA exchange plans, however, it's more like 5% of the total, or 1/20th.

A straight extrapolation of this suggests that the actual amount sitting in the segregated abortion funds could actually be as much as $500 million, although there's a host of variables I'm not taking into account: The average cost of an abortion varies by state, for instance; and of course there are some states where exchange plans are neither banned from nor required to cover abortion, which presumably means that some do & some don't.

In any event, it sounds like our long national nightmare of unused abortion funds has finally come to an end. Or something. So...hooray, I guess?

Advertisement