New KFF survey confirms everything I've been warning about for months.

Thu, 03/19/2026 - 5:18pm

For months now I've been warning that the initial data published about the 2026 ACA enrollment would likely massively underestimate just how ugly things were in terms of both effectuated enrollment as well as how comprehensive the coverage would be for those who did enroll.

Back in December, when Open Enrollment was still going on, I noted that regardless of what the official number of Americans who selected an exchange plan during Open Enrollment was, the actual number of those who would have effectuated coverage over the course of the year would likely be far lower:

So, what will this graph look like for 2026?

...IF that's what ends up happening, it would look something like the following:

- Total Open Enrollment QHP Selections: Perhaps ~23.3 million

- February 2026 Effectuation Total: Perhaps ~21 million

- December 2026 Effectuation Total: Perhaps ~17 million

Full-year average effectuations: Perhaps ~18.5 million, vs. the ~22.5 million I expect 2025 to average...or ~4 million fewer people with coverage on average for the year. This would be in line with the Congressional Budget Office's projection of 4.2 million losing coverage due to the enhanced tax credits expiring.

Again, this isn't a projection on my part; I honestly don't know exactly what it will look like. The main point to keep in mind is that CMS is unlikely to actually publish that data until sometime in July 2026 if at all, so any crowing by the Trump Administration, Congressional Republicans or their allies about the tax credits expiring having a "minimal impact" etc. should be taken with a massive grain of salt until then.

Well, it turns out that the initial plan selections were even lower than I speculated: Just over 23.0 million people, down around 1.3 million from OEP 2025. So, y'know, that's not great. There's been a few nuggets of additional data which have come in out of Maryland and Massachusetts regarding effectuated enrollment so far:

Maryland:

...even with only two months of data in for 2026, the early indicators aren't great: Effectuated enrollment in Maryland dropped 4.2% from January to February, a rate 75% higher than the Jan - Feb drop last year, and nearly 4x higher than it was from Jan - Feb 2024.

Massachusetts:

...I don't have the month-over-month percent drop displayed in the table this time, but from January - February 2026 effectuated enrollments dropped 3.7%, compared to a 4.1% increase month over month in 2025. Whoa.

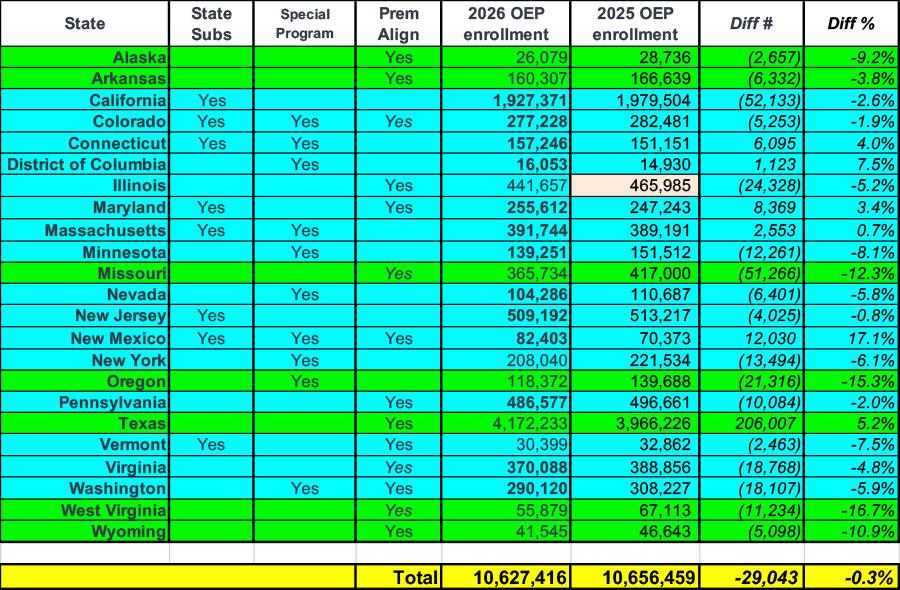

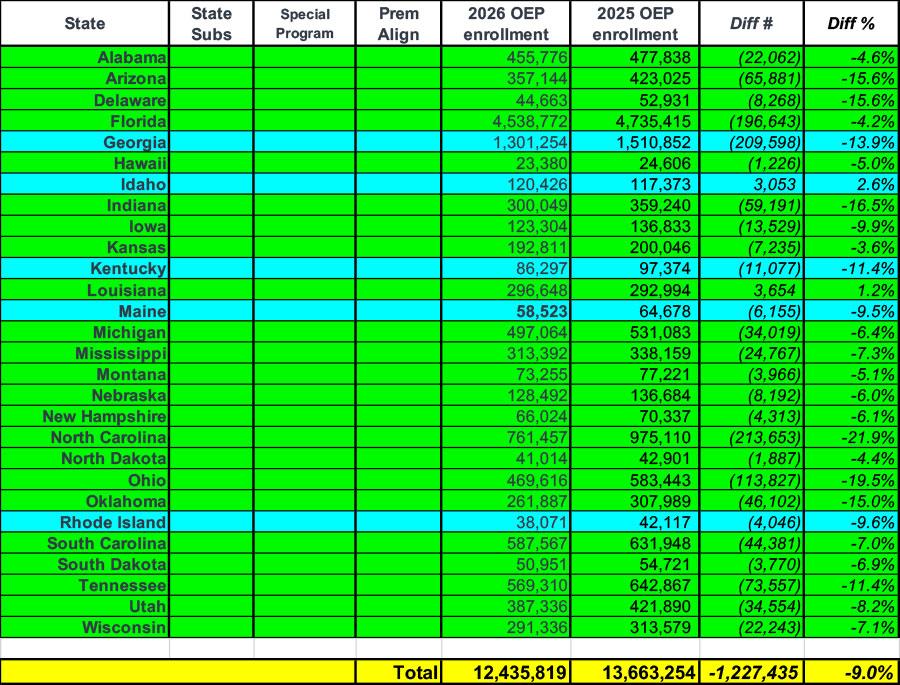

Keep in mind that both Maryland and Massachusetts have generous state-based subsidy programs in place which are almost certainly shoring up enrollment...programs which most states don't have. As I wrote last week, the 23 states which have at least some sort of special program in place to mitigate the damage (state-based subsidies, special programs for lower-income enrollees like BHPs, and/or Premium Alignment policies) only saw a nominal drop in enrollment overall (around 0.3%), while the 28 states which don't include any such programs saw plan selections drop by a whopping 9% out of the gate:

The other major warning I made in early January was that even for the ~23 million people who did go ahead and either re-enroll or newly enroll in an exchange plan for 2026, a large portion of them (my own family included) would almost certainly have to downgrade to a much worse plan, which means either a lower metal level (Gold to Silver, Silver to Bronze), a worse type of plan (PPO to HMO), a skinnier provider network or all of the above:

Hell, my own family did exactly this: We were forced to downgrade from a Silver PPO plan to a Bronze HMO plan in order to keep our premiums from increasing a whopping $17,000...but the trade-off for that is that our deductible just went up 150% (which we're virtually guaranteed to max out), meaning we're still very likely going to see our total healthcare costs skyrocket by over $15,000 this year.

The thing is, that extra $15,000 isn't gonna show up in the Center for Medicare & Medicaid Service's (CMS) "average net premium" calculation, since technically our premiums didn't go up at all.

Millions of other enrollees will still see their net premiums go up even if they downgrade their policies...it's just that it might be, say, a 40% increase instead of 200% or whatever.

Again, I posted a follow-up to this last month with some hard initial data (from a handful of states) which supported exactly what I feared:

When you combine all five states, this is what it looks like:

- Platinum plan enrollment has dropped nearly 11%

- Gold plan enrollment has dropped 8.1%

- Silver plan enrollment has dropped 8.8%

Silver/Gold/Platinum plans are down a combined 8.7%, while Bronze and Catastrophic plan enrollment are up a combined 23.8%.

Put another way, that's 197,000 fewer people with low-deductible plans and 162,000 more people with high-deductible plans.

And again, keep in mind that these are all states with various levels of additional financial support for enrollees. I can't begin to fathom what it's gonna look like in states like, say, Oklahoma, Tennessee or Indiana which don't have any such mitigating circumstances.

In any event, this morning KFF published the results of a follow-up survey to one they did last fall of well over 1,000 ACA exchange enrollees to see how they're faring today...and while this may not be completely representative, it pretty much lines up exactly with everything I've been predicting all along:

At the end of 2025, despite a government shutdown over the policy, the enhanced premium tax credits expired, decreasing financial assistance for subsidized Marketplace enrollees and contributing to significant increases in the Affordable Care Act (ACA) Marketplace costs for most enrollees overall. Amid the debates leading up to the expiration, KFF conducted a probability-based survey of 1,350 adults covered by ACA Marketplace plans in late 2025 to better understand their worries about potential cost increases for their health coverage. Now—without the enhanced tax credits in place—KFF re-interviewed 1,117 individuals (more than 80% of the original sample) to learn how they are navigating these changes to the ACA Marketplace.

This report is based on all 2025 Marketplace enrollees who took the follow-up survey, including returning Marketplace enrollees, those who have left the Marketplace entirely for another type of coverage, and those who are now uninsured.

From KFF's report:

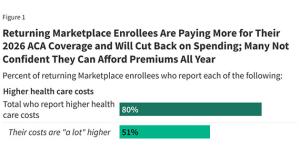

- 80% of all enrollees have higher overall healthcare costs (duh), with over 50% reporting much higher costs

- Over 70% are worried about being able to afford emergency care or hospitalizations

- Over half are being forced to cut back on other types of household spending to afford medical expenses

- 17% aren't confident that they'll be able to afford to pay their monthly premiums for the rest of 2026

Assuming this is representative nationally, that amounts to over 3.9 MILLION exchange enrollees who may be forced to drop their coverage partway through the year.

IMPORTANTLY, the survey also notes that...

Additionally, 4% of returning Marketplace enrollees say they have yet to pay their first premium for 2026. Notably, returning enrollees who receive tax credits to help pay for their coverage are generally provided with a 3-month grace period for nonpayment of premiums, meaning most may have until the end of March to pay any premiums that are due before facing the retroactive termination of their health insurance coverage.

According to KFF's methodology, the follow-up survey was conducted between February 12th - March 2nd, which means that these folks were surveyed after the 2026 Open Enrollment Period had ended in every state.

-

9% of those enrolled as of 2025 say that they are ALREADY currently uninsured

Remember, the official CMS report stated that just over 23.0 million people selected exchange plans for 2026...down around 5.2% from the 24.3 million who did so in 2025. This means that--again, assuming it's representative nationally--right out of the gate, the drop in effectuated enrollment is at least 73% higher than the CMS report suggested.

The original KFF survey was done in mid-November 2025. According to CMS's most recent Medicaid/CHIP report, total effectuated exchange enrollment was around 22.3 million at the time. If effectuated enrollment is down 9% from then, that would put it at around 20.3 million as of mid-February, give or take. This would be around 1.53 million fewer than February 2025 effectuations, FWIW.

If none of the 4% of 2025 enrollees who haven't paid their first 2026 premium yet end up doing so by the end of March, that extrapolates out to another ~920,000 who would lose coverage effective April 1st.

More significantly, however:

- 28% said that they've switched to a different exchange policy...and while some people switch plans every year, the reason is vitally important:

When asked the reasoning behind their change, a larger share say costs were the driver rather than changes to their health care needs. A 34-year-old man living in Texas put it this way, “The prices are simply too high. $800/month for the absolute cheapest plan for two people. Our income is $120k, so we don’t qualify for subsidies in Texas. I don’t think we could afford our mortgage if I had to pay for health insurance.”

According to KFF, 39% of last years enrollees remained in the same plan; 28% switched to a different plan; and 22% switched to a different type of healthcare coverage entirely. Again, while this happens to some degree every year as people age into Medicare, gain employer-sponsored coverage, fall below the Medicaid eligibility threshold etc, this year the expiration of the enhanced federal subsidies adds a much uglier factor to all of this.

- 7% moved to Medicaid

- 5% moved to non-ACA compliant coverage (see below)

- 5% moved to employer-based coverage

- 4% moved to Medicare

- 1% (presumably all under 26 yrs old) moved to their parents coverage (presumably via an employer)

KFF notes that fully half of 18 - 29 yr olds moved off of ACA exchange coverage this year...which is gonna be devastating to the risk pool since the remaining enrollees will be sicker & more expensive to treat as a result.

The 5% who moved to "non-ACA coverage" doesn't go into detail, but I'm guessing this mostly includes "junk plans" like so-called "Short-term, Limited Duration" plans; "Sharing Ministry" plans; "Farm Bureau" plans and so forth...which doesn't bode well.

As for those who switched to a different ACA exchange plan:

Eight in ten say they made a change to their coverage because it was too expensive, including seven in ten (71%) who say this was a “major reason” and one in ten (9%) who said it was a “minor reason.”

...About six in ten (63%) returning Marketplace enrollees say their monthly health insurance premium is higher than 2025, including 40% who say it is “a lot higher.” In addition, nearly half say their deductibles are higher (45%, including 24% who say they’re “a lot higher”), and one-third say their coinsurance and co-pays are higher compared to last year (36%, including 18% “a lot higher”).

Increases in insurance plan cost-sharing are pronounced among those who say they switched their Marketplace plan this year. Over half (54%) of returning enrollees who switched plans say their deductibles are higher this year compared to last year (including 34% who say “a lot higher”), and an additional four in ten (42%) say their coinsurance and co-pays are higher (25% “a lot higher”). This likely reflects the fact that some enrollees switched to lower tier Bronze plans which may mitigate some of the increase in premiums but typically have higher out-of-pocket costs. Overall, a quarter (26%) of plan switchers say they downgraded their metal plan (e.g. from a Silver plan to a Bronze plan) in 2026.

Bingo...that's exactly what my wife and I had to do.

There's a lot of other wonky data points in the full survey, but I'm gonna skip to the politics of it all:

...many who are registered to vote say that the cost of health care will have a major impact on their decision to vote (48%) and which party’s candidate they will support (49%) in the midterm elections. The issue currently resonates more with Democrats, who are more than twice as likely as Republicans to say health costs will play a major impact on their decision to vote in the 2026 midterms (67% vs. 27%) and on which candidate they decide to vote for (70% vs. 30%).

Overall, a whopping 78% of ACA exchange enrollees think the enhanced subsidies should have been extended (and I'm guessing many of the 20% who don't weren't subsidies to begin with...)...including 94% of Democrats, 80% of Independents and even 58% of Republicans. Hell, even 54% of self-described MAGA Republicans think so.

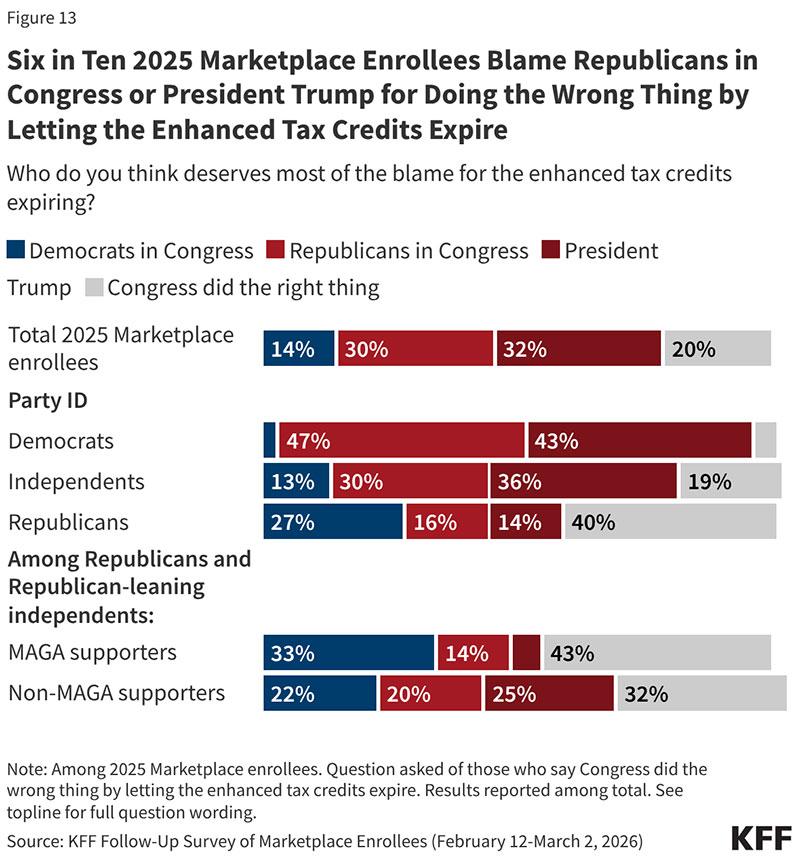

62% of enrollees blame Republicans for the subsidies expiring vs. just 14% who blame Democrats (which is still too high since every Democrat in both the House and Senate literally voted to keep them in place, but still).

Finally, and perhaps most critically:

...Three-quarters of 2025 Marketplace enrollees who are registered to vote say the cost of health care will have a “major impact” or “minor impact” on their decision to vote (73%) and which party’s candidate they will support (74%) in the midterm elections. Majorities of voters across partisanship say health care costs will impact their voting decisions, however Democrats are more than twice as likely as Republicans to say it will have a major impact on their decision of whether to vote (67% vs. 27%) and on which party’s candidate they will support (70% vs. 30%). At least four in ten independent voters say that health care costs will have a major impact on their decision to vote (47%) and who they decide to vote for (44%).

Advertisement